Leveraged Floored Floater

Floored Floaters

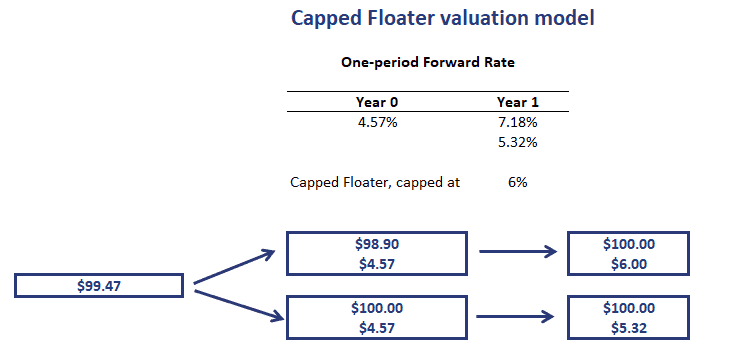

Valuation Capped Floater Breaking Down Finance

Callable Capped Floaters

Inverse Floaters Coupon Formula Calculation Example Why Investing

Ch0414250966 Cms Steepener 3y On Usd 10s2s Derinet Switzerland

/GettyImages-1147331105-b6d11d4d59a445c0909f2c61510df139.jpg)

Inverse Floater Definition

Leveraged floaters also require a floor since the coupon rate can never be negative.

Leveraged floored floater.

Introduction To Structured Products Srp Academy

Nuveen Preferreds Cefs Partially Releverage Seeking Alpha

Sinopartners Family Office Investments

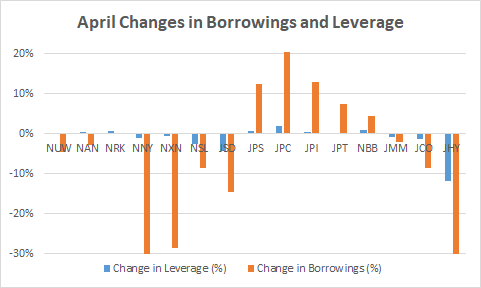

May 2019 Page 4

Jb Certificates And Warrants On Interest Rates In Eur Usd And Chf Pdf Free Download

Fixed Income Analysis 4th Edition Wiley

Cfa Level 3 2019 Trading Implementation Shortfall Part 1 Youtube

Https Www Research Unicredit Eu Docskey Creditstrategy Docs 2016 157026 Ashx Ext Pdf Key Sb2lbicthcbdthaw4ad Lvh9grmky7hu5xv6meyq4ja8yljjg6sbvg T 1

Derivatives Fincyclopedia

Products Interest Rates Plunging Derinet Switzerland

Xhmd4pzt Yntm

Products Sustainable Investment Products Derinet Switzerland

Https Derinet Vontobel Com Ch Download Assetstore Eb8fbf9a 537a 497c 9070 Ad16b9bcd213 Issuance Program 2018

Https Nanopdf Com Download Create A Model In Excel Vba To Value Floating Rate Notes Frn Pdf

Source : pinterest.com